Electronics Weekly

Electronics Weekly

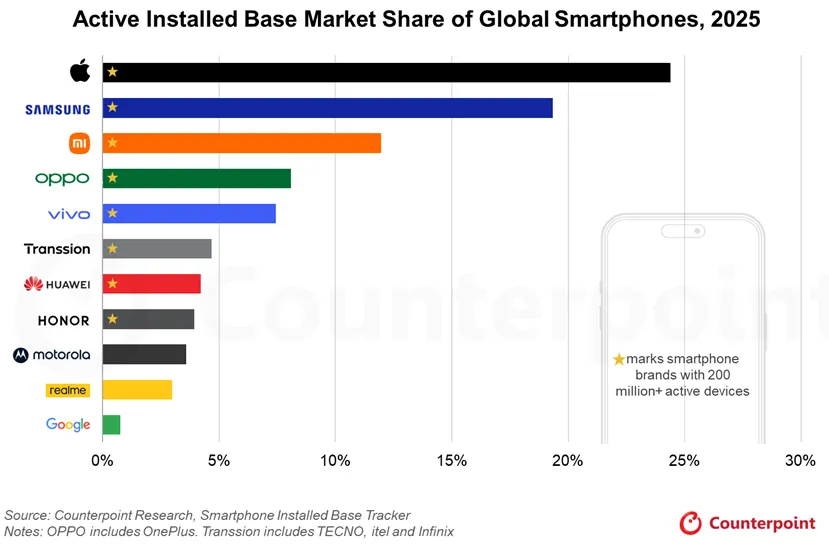

“Each of the eight leading smartphone OEMs had an active installed base exceeding 200 million devices in 2025, together accounting for over 80% of the global active installed base,” says Counterpoint’s Tarun Pathak, “only Apple and Samsung have surpassed the one-billion active devices milestone.”

The premium segment remains challenging. In 2025, six OEMs outside Apple and Samsung held only a single-digit sales share in the premium segment priced above $600 wholesale.

This highlights the difficulty of competing in this space. Further, while users are gradually moving to higher price bands, ongoing memory shortages are raising component costs and limiting the availability of higher-specification models.

This could delay upgrades, extend replacement cycles and slow the premiumization trend.

In the AI era, differentiation is shifting to software and ecosystem layers. On-device AI, camera intelligence, productivity features and seamless cross-device integration are becoming key value drivers.

These help build loyalty and increase usage. Growing the active installed base and extending device lifespans strengthen software revenue potential, turning each smartphone into a long-term monetisation platform.

Apple remains the only brand consistently generating high-margin revenues from its installed base, with services revenue continuing double-digit growth.

Longer software support and stronger ecosystem lock-in increase user lifetime value. As hardware growth slows and cost pressures rise, software and services offer OEMs a stable, recurring revenue stream less dependent on replacement cycles