Electronics Weekly

Electronics Weekly

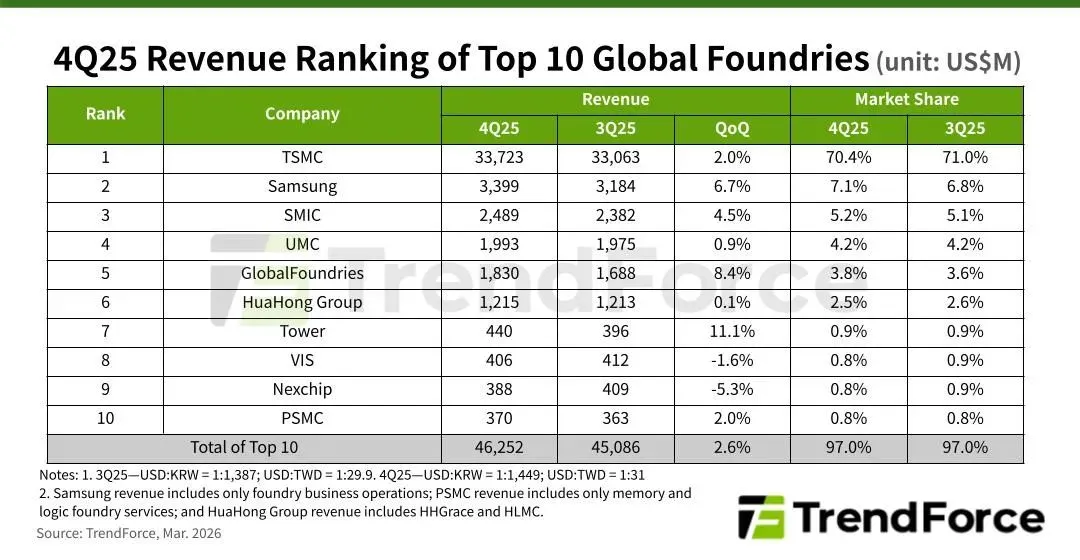

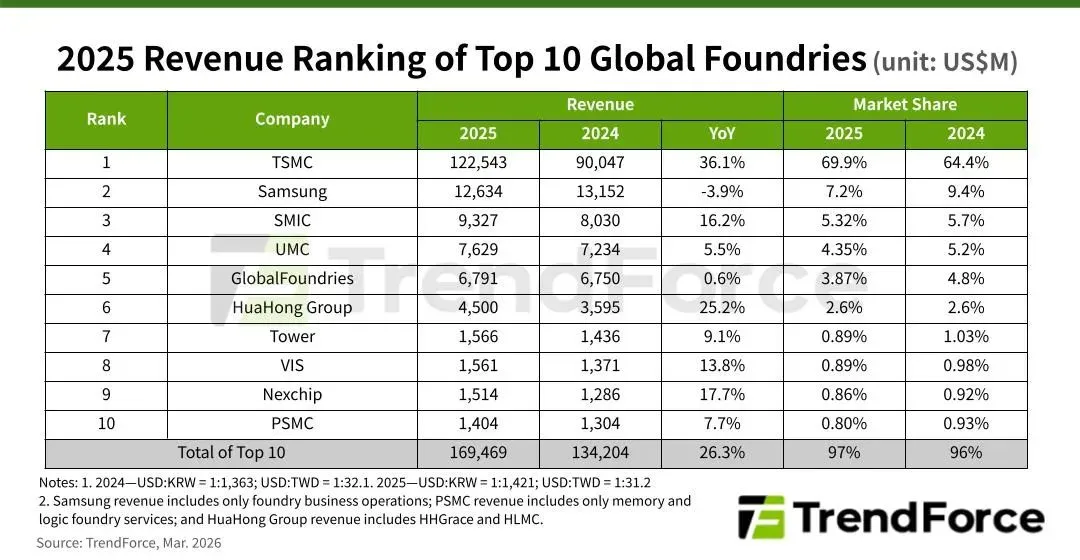

In Q4 the combined revenue of the world’s top ten foundries were up 2.6% QoQ to nearly $46.3 billion.

TSMC saw slightly lower wafer shipments in 4Q25, but 3nm smartphone wafers lifted ASP delivering a 2% QoQ revenue rise to $33.7 billion for a 70.4% market share.

Samsung Foundry (excluding System LSI) recorded 6.7% QoQ revenue growth to reach nearly $3.4 billion in 4Q25. Revenue was supported by shipments of new 2nm products, as well as the production of logic dies used in Samsung’s HBM4 memory. These contributions helped offset a slight decline in overall fab utilization. Samsung not only returned to profitability but also increased its market share from 6.8% to 7.1% to maintain second place.

SMIC ranked third as the company continued to benefit from localization demand. Revenue rose 4.5% QoQ to almost $2.49 billion, with growth driven by higher wafer shipments, slightly improved ASP, and additional photomask shipments toward the end of the year.

UMC remained fourth and revenue increased 0.9% QoQ to around $2 billion.

GlobalFoundries ranked fifth as wafer shipments and ASP improved, driving 8.4% QoQ revenue growth to $1.8 billion.

HuaHong Group ranked sixth. At its subsidiary HHGrace, demand for MCUs and PMICs lifted revenue 3.9% QoQ in 4Q25. After consolidating revenue from HLMC, HuaHong Group reported total revenue of approximately $1.22 billion, up 0.1% QoQ.

Tower’s semiconductor revenue rise 11.1% QoQ to $440 million, pushing the company ahead of Vanguard and Nexchip to take seventh place.

Vanguard ranked eighth, with revenue declining 1.6% QoQ to $406 million.

Nexchip claimed the ninth position, reporting a 5.3% QoQ drop in revenue to $388 million.

Finally, PSMC finished in tenth place with quarterly revenue rising 2% QoQ to approximately $370 million.