Electronics Weekly

Electronics Weekly

DMASS Europe‘s chairman, Hermann Reiter, said that after a “prolonged period of stagnation, the European electronic components market is showing the first signs of renewed momentum” but warned “structural dependencies and supply chain vulnerabilities remain a critical concern beside the fragmenting customer markets”.

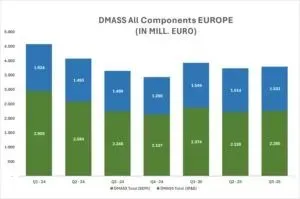

Semiconductor distribution rose 0.8% in Q3 2025 to reach a value of €2.26bn. Across Europe, however, the picture was mixed with only Benelux and Turkey growing at 10.3% and 27.4% respectively, while Israel, Switzerland, Eastern Europe, the UK and Iberia all saw falls compared to the same quarter last year.

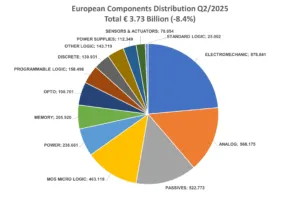

The strongest growth was in sensors and actuators (19%), memory (6.9%) and non-MOS micro logic (21.6%), while power dropped 10% and MOS micro logic fell 5.6%.

The IPE sector across Europe reached €1.53bn, an increase of 9.4%. Growth was strongest in Israel (42%) and Turkey (33%). The UK dropped (-1.6%) and growth was more modest in Ireland (4.6%) and Austria (2.5%), with Eastern Europe and Nordic maintaining mid-table positions with rises of 17.7% and 13.8% respectively.

Within this group, passive and e-mech components increased by over 8% each and power supplies increased 16.9%. Batteries and accumulators saw a steep decline of 9% and ceramic capacitors increased by 13%, but this was eclipsed by the 29% increase achieved by AC-DC converters.

“While this development provides a welcome signal of recovery,” said DMASS, “it must be viewed against the backdrop of persistent geopolitical tensions and the continent’s continued reliance on external sources for key technologies and materials. This dependency exposes Europe to volatility and underscores the fragility of global supply chains, which remain susceptible to political, economic, and logistical disruptions.”