Electronics Weekly

Electronics Weekly

Its forecast for 2026 is in a similar vein as global trade issues, such as trade tariffs, a decline in car manufacturing, slow economic growth across Europe and slowing growth rates in China, all make for uncertainty.

There are signs that in-house inventories are being consumed to reduce levels, but customers are reluctant to place longer term order cover, said ecsn‘s market analyst Aubrey Dunford (pictured).

Price increases in 2025 were more than unexpected across all global markets, he said. While there was a growing demand for applications, design inactivity remains strong. The lack of confidence in the market has delayed a lot of projects being released into production, he continued.

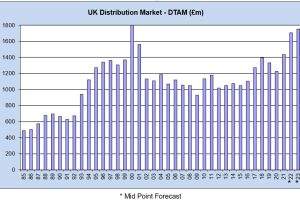

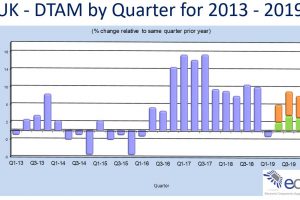

Single-digit billings of between 2% and 4.9% were predicted for 2025 and although audited figures are not yet available, indications are that 2025 will see a decline of 9%, due to continuing weak demand for components, exacerbated by the industry-wide inventory hang, said Adam Fletcher, chairman, ecsn.

In fact, the predictions for -5% in the first half of 2025 were optimistic. The first half of the year saw -13% and although this decline slowed in Q3, Dunford expects the overall demand will be -9% compared to 2024.

Factors limiting growth are a decline in manufacturing and in particular car production in Germany. The connector market, however, shows signs of growth, finding applications in electric vehicles. The military and aerospace markets remain strong for electronic components, but these are only a small part of the total market. The roll-out of 5G and infrastructure are also expected to contribute to demand. Looking further ahead, AI in mainstream computing, consumer, mobile handsets, industrial and medical equipment are likely to impact revenues in the next two to five years.

Regionally, revenue growth for semiconductors is strong, led by specialised memory products such as GPUs for AI applications.

For next year Dunford predicts modest growth of between 2% and 3%.